All Categories

Featured

2 individuals acquisition joint annuities, which provide a guaranteed revenue stream for the rest of their lives. When an annuitant dies, the rate of interest earned on the annuity is handled in different ways depending on the kind of annuity. A type of annuity that quits all repayments upon the annuitant's death is a life-only annuity.

The initial principal(the amount at first transferred by the moms and dads )has actually currently been exhausted, so it's not subject to tax obligations again upon inheritance. The incomes part of the annuity the rate of interest or investment gains accrued over time is subject to earnings tax. Normally, non-qualified annuities do.

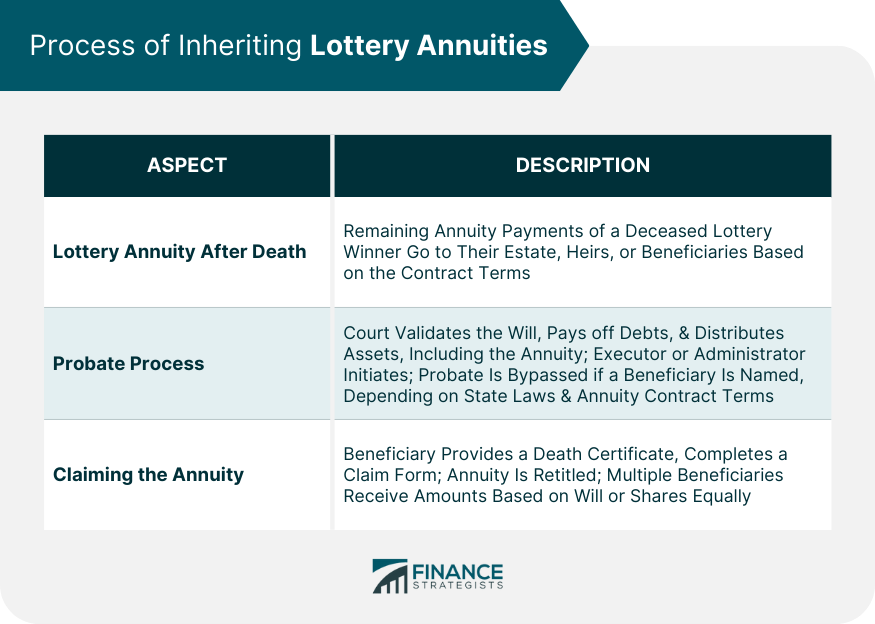

have died, the annuity's advantages usually change to the annuity proprietor's estate. An annuity owner is not lawfully called for to notify current beneficiaries concerning modifications to recipient designations. The choice to transform recipients is commonly at the annuity owner's discernment and can be made without notifying the existing recipients. Considering that an estate practically does not exist till an individual has actually passed away, this beneficiary designation would only enter into impact upon the death of the called person. Normally, once an annuity's proprietor dies, the designated beneficiary at the time of death is qualified to the advantages. The partner can not alter the recipient after the owner's death, also if the beneficiary is a minor. Nevertheless, there may specify provisions for taking care of the funds for a minor recipient. This often entails appointing a guardian or trustee to take care of the funds till the youngster maturates. Normally, no, as the beneficiaries are not accountable for your financial debts. It is best to seek advice from a tax obligation specialist for a details solution associated to your situation. You will remain to receive repayments according to the contract routine, yet trying to get a round figure or car loan is likely not an option. Yes, in nearly all instances, annuities can be acquired. The exemption is if an annuity is structured with a life-only payment choice with annuitization. This kind of payment ceases upon the fatality of the annuitant and does not supply any recurring worth to heirs. Yes, life insurance policy annuities are generally taxed

When taken out, the annuity's earnings are taxed as regular earnings. The primary amount (the first financial investment)is not strained. If a recipient is not called for annuity benefits, the annuity continues normally most likely to the annuitant's estate. The circulation will adhere to the probate procedure, which can delay repayments and might have tax obligation effects. Yes, you can name a trust as the recipient of an annuity.

Are Immediate Annuities death benefits taxable

This can provide greater control over just how the annuity benefits are dispersed and can be part of an estate preparation strategy to manage and safeguard assets. Shawn Plummer, CRPC Retired Life Organizer and Insurance Coverage Representative Shawn Plummer is a licensed Retirement Organizer (CRPC), insurance coverage representative, and annuity broker with over 15 years of direct experience in annuities and insurance policy. Shawn is the creator of The Annuity Professional, an independent on the internet insurance coverage

firm servicing consumers throughout the USA. Through this platform, he and his group objective to eliminate the guesswork in retired life preparation by assisting individuals discover the best insurance policy coverage at one of the most competitive prices. Scroll to Top. I comprehend all of that. What I do not comprehend is how before getting in the 1099-R I was revealing a refund. After entering it, I currently owe tax obligations. It's a$10,070 distinction in between the reimbursement I was expecting and the taxes I currently owe. That appears really extreme. At the majority of, I would have anticipated the refund to decrease- not totally go away. A financial expert can aid you choose just how finest to manage an inherited annuity. What occurs to an annuity after the annuity proprietor dies relies on the terms of the annuity agreement. Some annuities merely stop distributing revenue settlements when the owner dies. In a lot of cases, nonetheless, the annuity has a survivor benefit. The recipient might obtain all the staying money in the annuity or an assured minimum payment, typically whichever is greater. If your parent had an annuity, their agreement will certainly define who the beneficiary is and might

right into a pension. An acquired individual retirement account is a special retirement account made use of to distribute the properties of a dead person to their beneficiaries. The account is signed up in the dead individual's name, and as a recipient, you are not able to make additional payments or roll the acquired IRA over to another account. Just qualified annuities can be rolledover into an acquired IRA.

{kind=link}

Latest Posts

Highlighting Fixed Vs Variable Annuity Pros Cons A Closer Look at How Retirement Planning Works Breaking Down the Basics of Fixed Index Annuity Vs Variable Annuity Features of Variable Annuity Vs Fixe

Breaking Down Fixed Vs Variable Annuity Key Insights on Your Financial Future Defining the Right Financial Strategy Features of Annuities Variable Vs Fixed Why Choosing the Right Financial Strategy Is

Highlighting Variable Annuity Vs Fixed Annuity A Comprehensive Guide to What Is A Variable Annuity Vs A Fixed Annuity What Is the Best Retirement Option? Benefits of Choosing the Right Financial Plan

More

Latest Posts